Tuesday, August 27, 2013

Economic Gains - Concept or Reality?

Don't want to be a "debbie downer" here but I came across this article in Logistics Management Magazine titled: Economic Gains are Sometimes More of a Concept Than Reality. I tend to agree with the author on this one and said as much in my Macroeconomic Monday post last week.

Monday, August 26, 2013

Is Domestic Oil Drilling The Right Security Policy for the US?

This is a topic near and dear to logisticians and the overall energy strategy for the United States which then translates into what supply chains can expect for energy policy. You cannot pick up a magazine, newspaper or watch a news show without the discussion of "energy independence" and how wonderful that will be / is for the United States. And it is precisely that popularity which causes me to seek out other opinions.

A person once said if two people always agree with each other then probably one is not thinking. The hoard mentality of energy independence makes me think that there must be another opinion - another way to look at things. Well, leave it to Charlie Munger, Warren Buffett's great partner, and some may say the brains behind Warren, to give me that other way of looking at things.

In looking at this idea of energy policy he brings us to a core question: Is it in the United States' best interest to "drain" the US now or should we in fact follow a policy of "drain the rest of the world" first and save our precious resource for the future? A different way of looking at this problem. In order to believe that you may want to drain the rest of the world first you probably believe:

This is truly a fascinating position which challenges the common thought of drill in the US first. He made me think: Why should we drill now? Oil in the ground is money in the bank and given that the ultimate price will be a global price to the consumer (i.e, the economy and the consumer see no benefit of local drilling) and that oil drilled in the US will be refined and then probably exported to equalize the global price, the correct policy is probably what Munger suggests - drain the rest of the world.

The only argument against this policy would be that we somehow benefit from local drilling and by the time we are drained there will be some type of substitute so it does not matter. To this argument I reply with the knowledge of Pascal's wager.

When Pascal was asked why he believed in God he basically said it was an exercise in probability. Basically he said he believed in God because if it turns out God does not exist than he really has lost nothing by believing in God during his life. However, if God does exist than it certainly was good he believed and for those who did not, they are looking at an eternity of flames.

So, let's apply this to Munger's ideas. If he is wrong, we have not lost anything (assuming we did not have to sacrafice mightly to drill the rest of the world). If he is right, we will have ensured the security of our children for hundreds of years after the rest of the world is drained.

Makes you think.

Ht: The Motley Fool

Watch the entire talk here: 21st Century annual Conference - ROUNDTABLE III Charlie Munger starts making his comments on energy policy at about 36 minutes in.

A person once said if two people always agree with each other then probably one is not thinking. The hoard mentality of energy independence makes me think that there must be another opinion - another way to look at things. Well, leave it to Charlie Munger, Warren Buffett's great partner, and some may say the brains behind Warren, to give me that other way of looking at things.

In looking at this idea of energy policy he brings us to a core question: Is it in the United States' best interest to "drain" the US now or should we in fact follow a policy of "drain the rest of the world" first and save our precious resource for the future? A different way of looking at this problem. In order to believe that you may want to drain the rest of the world first you probably believe:

- At some point, oil will become a scarce commodity. This is not a popular view right now as we have moved from "peak oil" to an environment of oil abundance. But, while we may argue about when, I think it is reasonable to believe that some day oil will be scarce.

- You have to believe that there will not be a replacement for oil when the scarce time comes.

If you believe those two items then the right policy is actually quite clear: drain the rest of the world first. While we can afford it and before the world catches on to us we should drain the world, even if it means drilling oil and bringing it to the US just to store then wait and see. Here are some comments from Charlie:

"Oil is absolutely certain to become incredibly short in supply and very high priced .. The imported oil is not your enemy, it's your friend. Every barrel that you use up that comes from somebody else is a barrel of your precious oil which you're going to need to feed your people and maintain your civilization. And what responsible people do with a Confucian ethos is suffer now to benefit themselves and their families and their countrymen later. The way to do that is to go very slow in producing domestic oil and not mind at all if we pay prices that look ruinous for foreign oil. It's going to get way worse later ...

The oil in the ground that you're not producing is a national treasure ... It's not at all clear that there's any substitute [for hydrocarbons]. When the hydrocarbons are gone, I don't think the chemists are going to be able to just mix up a vat and create more hydrocarbons. It's conceivable that they could, I suppose, but it's not the way to bet. We should spend no attention to these silly economists and these silly politicians that tell us to become energy independent.

Let me pose a question for you. It's 1930. Oil in the United States is in glut. We have cartels to get the price up to $0.50 a barrel. Everywhere we drill we find more oil in our own country; everywhere we drill in Arabia we find even more.

What would the correct policy of the United States have been in that time? Well, the correct policy would have been to issue $150 billion of very long-term bonds and cart 150 billion barrels of Middle Eastern oil into the United States and throw it into our salt caverns and leave it there untouched until the current age.

It's easy to see that in retrospect, but who do you see who ever points this out? Zero. We have a brain-block on this issue. We should behave now to do on purpose what we did on accident then."

This is truly a fascinating position which challenges the common thought of drill in the US first. He made me think: Why should we drill now? Oil in the ground is money in the bank and given that the ultimate price will be a global price to the consumer (i.e, the economy and the consumer see no benefit of local drilling) and that oil drilled in the US will be refined and then probably exported to equalize the global price, the correct policy is probably what Munger suggests - drain the rest of the world.

The only argument against this policy would be that we somehow benefit from local drilling and by the time we are drained there will be some type of substitute so it does not matter. To this argument I reply with the knowledge of Pascal's wager.

When Pascal was asked why he believed in God he basically said it was an exercise in probability. Basically he said he believed in God because if it turns out God does not exist than he really has lost nothing by believing in God during his life. However, if God does exist than it certainly was good he believed and for those who did not, they are looking at an eternity of flames.

So, let's apply this to Munger's ideas. If he is wrong, we have not lost anything (assuming we did not have to sacrafice mightly to drill the rest of the world). If he is right, we will have ensured the security of our children for hundreds of years after the rest of the world is drained.

Makes you think.

Ht: The Motley Fool

Watch the entire talk here: 21st Century annual Conference - ROUNDTABLE III Charlie Munger starts making his comments on energy policy at about 36 minutes in.

Wednesday, August 21, 2013

In Memory of A True Visionary - John "Jock" Menzies

Unfortunately I was greeted this morning with news of his untimely death. I ask myself why we seem to lose the great ones far too early and when they have far more to contribute. But, alas, that is not a question for me to answer.

I just mark myself as part of a very lucky and fortunate group who had the pleasure of having breakfast with Jock and listening to his fascinating story and sharing in his vision. The works on the ALAN website this morning said it best:

"May we honor his memory - and celebrate his life - by listening more carefully, responding more positively, and living more gently with one another. Perhaps together we can retrieve some small portion of the grace we have lost with his premature passing"

John "Jock" Menzies will be missed.

Saturday, August 17, 2013

Tesla Motors' Supply Chain VP to Speak at CSCMP Annual Global Conference; Closing Session to Focus on Personal Development

Tesla Motors' Supply Chain VP to Speak at CSCMP Annual Global Conference; Closing Session to Focus on Personal Development

A great development and looking forward to this fantastic discussion. How to design and make a supply chain from scratch!

A great development and looking forward to this fantastic discussion. How to design and make a supply chain from scratch!

Macroeconomic Monday® - The Demographic Shift to Multi Family, City Dwelling is Real

For those reading this today, Saturday, I normally write this on Saturday then post on Monday. But, I figured if you want to read on Saturday why not? However, the name remains the same.

So, last week was an incredible week for economic news and the stock market. I remind everyone who may think the financial sky is falling that the S&P is still up close to 18% this year so I would not fret too much (Unless you are a late comer to the party then you may wonder what happened). From a purely financial point of view this week was bound to happen. Call it reversion to the mean, a short correction or whatever you want the bottom line is stocks cannot just keep going up forever. The curve is not smooth and if you want it to be smooth then you are involved in the wrong business.

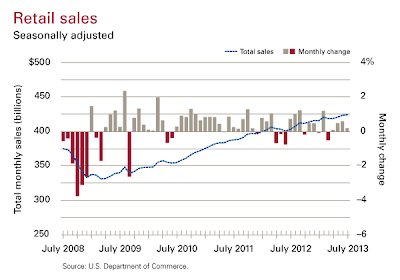

But, there were some very interesting dynamics. First, retail spending continues to be softer than the analysts predicted. Sometimes I wonder if the analysts are really forecasting or are they hoping - I have said all along that until unemployment changes significantly (i.e. at 6% or below), retail is going to suffer. Yes, there are some "must have" items which hit a replacement cycle (Cars and appliances) that you just have to replace no matter what. But, the discretionary is where consumers just are not going to spend their money. The graph to the right outlines the anemic changes in retail sales and it shows a very variable and anemic growth for retail sales. My readers know I do not buy into this "weather" blame game people make for why this is adjusted. The bottom line is it just looks like people are buying essentially what they need.

But, there were some very interesting dynamics. First, retail spending continues to be softer than the analysts predicted. Sometimes I wonder if the analysts are really forecasting or are they hoping - I have said all along that until unemployment changes significantly (i.e. at 6% or below), retail is going to suffer. Yes, there are some "must have" items which hit a replacement cycle (Cars and appliances) that you just have to replace no matter what. But, the discretionary is where consumers just are not going to spend their money. The graph to the right outlines the anemic changes in retail sales and it shows a very variable and anemic growth for retail sales. My readers know I do not buy into this "weather" blame game people make for why this is adjusted. The bottom line is it just looks like people are buying essentially what they need.

The other big event was the move in the 10 year note. This graph is even more telling about what is going on in the economy where you can see the interest rates are spiking fast.

The 10 yr T-Note of course is what a lot of mortgages are tied to which drives the housing market. This is another "KPI" I monitor for the economy. If the 10 year T-Note gets above 3% watch out!

The 10 yr T-Note of course is what a lot of mortgages are tied to which drives the housing market. This is another "KPI" I monitor for the economy. If the 10 year T-Note gets above 3% watch out!

Yes, I know and have heard many say that these are incredibly artificially low interest rates and so going above 3% is more of a reversion back to the mean or the norm. My response channels the blog posting I made recently about Nate Silver and the idea of "out of sample". Yes, in normal times the 10 Year T-Note should be at 3.5% to 4% and we should be able to live with it. However these are not normal times. We are above 7% unemployment, we are coming off of the worst recession (some say depression) since the 1930's and even for those employed many are dramatically underemployed. So, imagine a scenario where you have 7% or above unemployment AND interest rates above 4%? That is not a good indicator for the economy.

Finally, this leads to the behavior of the home buyer. They are not buying. What they are doing is moving into multi family dwellings. While multifamily dwellings increased over 26%, the building of single family homes declined by 2.2%. On average people spend more money on other things (think lawnmowers, curtains, a lot more furniture, nicer appliances etc. etc.) when they move into single family homes rather than when they move into multi family homes. This will be a net drag on the overall consumer spending numbers even though it will keep the builders busy for a short period of time.

So, in summary, we have a situation where the consumer has closed their wallet, interest rates are rising, single family homes are in decline. All speaks for a sluggish economy with some bright spots (autos for example). Freight will remain low (especially after these retail numbers) and hopefully the continued rise in 10 Year T-Notes will not choke off any semblance of recovery we may have going.

So, last week was an incredible week for economic news and the stock market. I remind everyone who may think the financial sky is falling that the S&P is still up close to 18% this year so I would not fret too much (Unless you are a late comer to the party then you may wonder what happened). From a purely financial point of view this week was bound to happen. Call it reversion to the mean, a short correction or whatever you want the bottom line is stocks cannot just keep going up forever. The curve is not smooth and if you want it to be smooth then you are involved in the wrong business.

But, there were some very interesting dynamics. First, retail spending continues to be softer than the analysts predicted. Sometimes I wonder if the analysts are really forecasting or are they hoping - I have said all along that until unemployment changes significantly (i.e. at 6% or below), retail is going to suffer. Yes, there are some "must have" items which hit a replacement cycle (Cars and appliances) that you just have to replace no matter what. But, the discretionary is where consumers just are not going to spend their money. The graph to the right outlines the anemic changes in retail sales and it shows a very variable and anemic growth for retail sales. My readers know I do not buy into this "weather" blame game people make for why this is adjusted. The bottom line is it just looks like people are buying essentially what they need.

But, there were some very interesting dynamics. First, retail spending continues to be softer than the analysts predicted. Sometimes I wonder if the analysts are really forecasting or are they hoping - I have said all along that until unemployment changes significantly (i.e. at 6% or below), retail is going to suffer. Yes, there are some "must have" items which hit a replacement cycle (Cars and appliances) that you just have to replace no matter what. But, the discretionary is where consumers just are not going to spend their money. The graph to the right outlines the anemic changes in retail sales and it shows a very variable and anemic growth for retail sales. My readers know I do not buy into this "weather" blame game people make for why this is adjusted. The bottom line is it just looks like people are buying essentially what they need.The other big event was the move in the 10 year note. This graph is even more telling about what is going on in the economy where you can see the interest rates are spiking fast.

The 10 yr T-Note of course is what a lot of mortgages are tied to which drives the housing market. This is another "KPI" I monitor for the economy. If the 10 year T-Note gets above 3% watch out!

The 10 yr T-Note of course is what a lot of mortgages are tied to which drives the housing market. This is another "KPI" I monitor for the economy. If the 10 year T-Note gets above 3% watch out!Yes, I know and have heard many say that these are incredibly artificially low interest rates and so going above 3% is more of a reversion back to the mean or the norm. My response channels the blog posting I made recently about Nate Silver and the idea of "out of sample". Yes, in normal times the 10 Year T-Note should be at 3.5% to 4% and we should be able to live with it. However these are not normal times. We are above 7% unemployment, we are coming off of the worst recession (some say depression) since the 1930's and even for those employed many are dramatically underemployed. So, imagine a scenario where you have 7% or above unemployment AND interest rates above 4%? That is not a good indicator for the economy.

Finally, this leads to the behavior of the home buyer. They are not buying. What they are doing is moving into multi family dwellings. While multifamily dwellings increased over 26%, the building of single family homes declined by 2.2%. On average people spend more money on other things (think lawnmowers, curtains, a lot more furniture, nicer appliances etc. etc.) when they move into single family homes rather than when they move into multi family homes. This will be a net drag on the overall consumer spending numbers even though it will keep the builders busy for a short period of time.

So, in summary, we have a situation where the consumer has closed their wallet, interest rates are rising, single family homes are in decline. All speaks for a sluggish economy with some bright spots (autos for example). Freight will remain low (especially after these retail numbers) and hopefully the continued rise in 10 Year T-Notes will not choke off any semblance of recovery we may have going.

Thursday, August 15, 2013

Wal-Mart Guides Lower - Sales Weaker

Reporting this morning, Wal-Mart is describing slow sales, and it has guided the street lower for the remainder part of the year. This is not good news but not unexpected for my readers. Until unemployment gets to 6% or lower you can expect to see a slow tough slog on consumer goods and that will deflate the demand for trucks. If you have to continue to look at one economic number which ultimately will drive the demand for transportation, look at unemployment.

If Wal-Mart guides down 1.5% to 3%, which is roughly what the news is saying this morning, that is a lot of empty trucks and containers on the road looking for freight.

Consumer durables appears to still be a strong point in the market but overall the story of a tough slog continues to hold true.

If Wal-Mart guides down 1.5% to 3%, which is roughly what the news is saying this morning, that is a lot of empty trucks and containers on the road looking for freight.

Consumer durables appears to still be a strong point in the market but overall the story of a tough slog continues to hold true.

Tuesday, August 13, 2013

Application of "Signal and The Noise" to Predicting Freight Volumes

I am deep into reading Signal and The Noise by Nate Silver - This is the guy who almost perfectly predicted the outcome of the last election, state by state, while virtually all of the talking heads and big public polling houses go tit all wrong. I have not finished the book yet but so far it is a fascinating read.

by Nate Silver - This is the guy who almost perfectly predicted the outcome of the last election, state by state, while virtually all of the talking heads and big public polling houses go tit all wrong. I have not finished the book yet but so far it is a fascinating read.

So, why discuss this on a transportation, logistics and supply chain blog? As many of you know, I am a closet forecaster. I use my data I observe and report on in my Macroeconomic Monday feature to try to determine what will happen in the transportation markets. I have my ups and downs and so far, however, I would say I have been far more accurate than the official transportation pundits (Magazines which are essentially paid for by the trucking industry, analysts who "cover" the industry but in reality are just trying to push stock prices up.. etc.) who have, for the last few years, reported a dramatic speed up in freight, a dramatic drop off in capacity and a huge inbalance driving rates up. I am sure they will be right one day but for now, if you had listened to them instead of me three years ago, you would have been paying far higher rates than you should have been.

Nate Silver describes a phenomenon in the book which I think is one of the core reasons why some of my predictions have been just a bit more accurate. The concept is that of being "Out of Sample". What this means is people will apply previous history to future results yet they will not realize enough data has changed which causes their examples they are using to not be representative of the current situation. So, the general belief that when the economy "heats up" there will be a problem with capacity fails to account for:

So, why discuss this on a transportation, logistics and supply chain blog? As many of you know, I am a closet forecaster. I use my data I observe and report on in my Macroeconomic Monday feature to try to determine what will happen in the transportation markets. I have my ups and downs and so far, however, I would say I have been far more accurate than the official transportation pundits (Magazines which are essentially paid for by the trucking industry, analysts who "cover" the industry but in reality are just trying to push stock prices up.. etc.) who have, for the last few years, reported a dramatic speed up in freight, a dramatic drop off in capacity and a huge inbalance driving rates up. I am sure they will be right one day but for now, if you had listened to them instead of me three years ago, you would have been paying far higher rates than you should have been.

Nate Silver describes a phenomenon in the book which I think is one of the core reasons why some of my predictions have been just a bit more accurate. The concept is that of being "Out of Sample". What this means is people will apply previous history to future results yet they will not realize enough data has changed which causes their examples they are using to not be representative of the current situation. So, the general belief that when the economy "heats up" there will be a problem with capacity fails to account for:

- Growth in intermodal

- Smaller packaging and product

- Movement of people to cities

- Software and collaboration models

- 3D printing

- The fact that more and more of GDP is not product driven but services and financial driven

And I am sure a lot more. My point here is that those who just extrapolate previous history to the future are doomed to have a failed prediction - my predictions seem to be a bit better because I am accounting for changes the external environment and accounting for them in my models.

To be clear, this may and most likely will change however for now I say (as I have for almost two years now) say that capacity / demand is fairly balanced and you should act that way. In the words of John Maynard Keynes, "When the facts change, I change my mind". I will keep my eye on the facts and will change my mind but one thing I will continue to work on is making sure I do not succumb to being "out of sample."

Monday, August 5, 2013

Why You, The Logistics and Supply Chain Manager, Need to OWN Your Sustainability Program

Many companies have sustainability offices or offices for Corporate Social Responsibility (CSR) and because of this many logistics and supply chain managers acquiesce their obligation to sustainability to these offices. The offices do not have the staff to really do the job at the execution level (they are great at setting high level goals and making press releases) and therefore much of a company's sustainability program is thrown over the wall to external "validating" agencies.

Looks like a good strategy right? After all, if you can say you are working with LEED or Smartway isn't that enough? Well the answer turns out to be no and the supply chain manager who does this does it at her own potential peril.

In a recent article the New Republic highlighted an example of this as it relates to LEED certification of the Bank of America building in New York. In this case, the investigative journalist found the building, while certified when it was empty, in practice is not very "green" at all. Read: In the EXECUTION of the sustainability program, it failed miserably.

Also notice the headline had Bank of America prominently displayed. The brand under attack in the headline was not the LEED brand (although deep in the article it did not fair well) but it was the actual company brand. This is important because one of the critical success factors of all sustainability programs at the execution level is brand protection. Imagine this scenario:

Looks like a good strategy right? After all, if you can say you are working with LEED or Smartway isn't that enough? Well the answer turns out to be no and the supply chain manager who does this does it at her own potential peril.

In a recent article the New Republic highlighted an example of this as it relates to LEED certification of the Bank of America building in New York. In this case, the investigative journalist found the building, while certified when it was empty, in practice is not very "green" at all. Read: In the EXECUTION of the sustainability program, it failed miserably.

Also notice the headline had Bank of America prominently displayed. The brand under attack in the headline was not the LEED brand (although deep in the article it did not fair well) but it was the actual company brand. This is important because one of the critical success factors of all sustainability programs at the execution level is brand protection. Imagine this scenario:

- Your CEO is out on the speaking circuit touting the sustainability and social responsibility of your company. Indeed, she is making this a cornerstone of why consumers should deal with your product.

- You feel like you are doing your job because your distribution centers are LEED certified and you at least ask your carriers if they are in the Smartway program.

- Someone now takes an inventory of what is really happening and they find out many of these "certifications" are so general in nature that they cannot be used to determine anything. A true and real inventory shows not much progress in truly reducing greenhouse gas emissions.

- An aggressive reporter or investator starts questioning your CEO about this - she looks perplexed

At that point the brand damage is done. All you are doing is playing catch-up to the damage and hoping time and some counter communication will work. You can find yourself with a real problem at this point.

Here are some recommendations to ensure this does not happen to you or to your company (and of course to your CEO):

- Take Ownership of Your Supply Chain Sustainability Program - The corporate office sets targets and high level goals and may be the location you send reports to but you must own the supply chain performance of this. Not some other office in your company and not some external agency.

- Employ external expertise as needed - This may sound contradictory but it is not. When I say use this external expertise I mean to actually dive in and inventory. This external agency should have no vested interest in the outcome beyond inventorying your GhG emissions, consulting with you on programs to reduce, developing road-maps and re-inventorying. They have a fiduciary responsibility only to you.

- Put goals and targets on performance appraisals with equal weight to other items - This is not and either/or as it relates to a sustainability program v. financial performance - it is a both. You must evaluate people on the actual performance of the program or they will only see it as a sideshow. Sideshows lead to results shown above.

- When conducting your inventory do it at a very detailed level - There are a lot of generic databases out in the public domain which say, essentially, "on average" this is what the emissions are for a company doing what you do. However, a lot of people have drowned in streams that "average" 3 feet deep. You must inventory at the truck, fleet and fuel level. Real consumption data for energy is a must. The higher you generalize the more likely it is your CEO will be surprised one day.

If you do not take ownership of your supply chain sustainability program with the same vigor and thoughtfulness you put against financial performance I can assure you someone else will... and that will not be the best day of your life.

If you still do not believe me think about how your company deals with safety. If someone asked you who is responsible for safety in your company would you really respond, "The safety office"? I think that makes my point.

XPO Logistics Starts a 8m Share Secondary Offering

The company says this is to help finance the previously announced acquisition of 3PD. As I said in a previous post, this acquisition seems to be more about taking 3PD public than synergies.

I don't pretend to be a financial genius but I am always suspect of selling part of a company and diluting earnings to current shareholders. Seems like if you really believe in the pro-forma you would want to keep as much as you can for yourself.

Friday, August 2, 2013

Can We Finally Get on With Life? HOS is Upheld

Today it was reported that virtually all of the provisions in the hours of service (HOS) rule-making were upheld in court (again). We should now be able to just get on with life, stop enriching the lawyers, and start planning our supply chains better.

Thursday, August 1, 2013

What Does 1.7%GDP Growth Mean for Transportation?

This week the first look at Q2 GDP came in and the number was 1.7%. Headlines were anywhere from "GDP Crushes Expectations" (Set the bar low) to "GDP Hardly Booming but no swoon in sight". The key factor for which headline you believe is what were your expectations to start with? Personally, I am in the camp that regardless, 1.7% is very anemic growth rate, it will not solve our unemployment problem and it will keep our economy somewhat mired for a long time.

But, what does it mean for transportation? I believe this is just another indicator to show demand is very tepid and will remain that way for some time. Revisions for GDP growth in Q1 were revised downward which means my experience meter seemed to have a better handle on GDP than the experts (I just look around and talk to people - Q1 was clearly worse than people had said). The Q1 number was revised down from 1.8% to 1.1%. Last three quarters have been less than 2% growth in each quarter.

For transportation this translates into lower demand and while there may be a little bit of capacity issues due to hours of service (HOS), demand is going down faster than capacity so net-net we are at balance or, in fact, slightly over capacity. In total we are seeing real overcapacity in intermodal as the big rush to get into that space has caused a huge container growth at the various IMCs.

The story from the transportation economists a few years ago was when you see 3% GDP growth that is when transportation rates will start going up. Of course, they have now changed that tune since 3% isn't anywhere near possible in the near future so the fear game is on hours of service.

However, my advice continues to be: Those who do not allow emotion, fear and "the government regulation boogey man" get to them will use real data to determine what is really happening. They will find capacity is there, rates are steady and in some cases going down, and for the foreseeable future that will be the story.

Keep calm and be diligent about your data analysis and you will find, while low GDP is not what we want for other reasons, this is probably a good time to be a buyer of transportation. If you stay calm while your competitors panic, you really can pick up some competitive advantage points during this period.

But, what does it mean for transportation? I believe this is just another indicator to show demand is very tepid and will remain that way for some time. Revisions for GDP growth in Q1 were revised downward which means my experience meter seemed to have a better handle on GDP than the experts (I just look around and talk to people - Q1 was clearly worse than people had said). The Q1 number was revised down from 1.8% to 1.1%. Last three quarters have been less than 2% growth in each quarter.

For transportation this translates into lower demand and while there may be a little bit of capacity issues due to hours of service (HOS), demand is going down faster than capacity so net-net we are at balance or, in fact, slightly over capacity. In total we are seeing real overcapacity in intermodal as the big rush to get into that space has caused a huge container growth at the various IMCs.

The story from the transportation economists a few years ago was when you see 3% GDP growth that is when transportation rates will start going up. Of course, they have now changed that tune since 3% isn't anywhere near possible in the near future so the fear game is on hours of service.

However, my advice continues to be: Those who do not allow emotion, fear and "the government regulation boogey man" get to them will use real data to determine what is really happening. They will find capacity is there, rates are steady and in some cases going down, and for the foreseeable future that will be the story.

Keep calm and be diligent about your data analysis and you will find, while low GDP is not what we want for other reasons, this is probably a good time to be a buyer of transportation. If you stay calm while your competitors panic, you really can pick up some competitive advantage points during this period.

Subscribe to:

Posts (Atom)