I realized some may not know of my twitter feed which is now up to close to 8K VERIFIED followers (have to go through a verification process to prevent robots from following). I "micro blog" at that site a lot more frequently. The link is:

https://twitter.com/Logisticsexpert

Sunday, August 9, 2015

Sunday, August 2, 2015

UPS Buys Coyote Logistics - No Surprise to Readers of 10x Logistics

This week, after a few weeks of rumors, we learned that UPS Paid $1.8bl for Coyote Logistics. This was no surprise to any reader of this blog as back in January of 2012 I wrote a post titled "The New Face of Brokerage". In this post I opined that Coyote Logistics was something unique and new and was not the "old" brokerage company. Great technology, great leadership and a "kick ass" attitude makes it one of the best. This week UPS realized this.

I also questioned in July of 2013 whether XPO's purchase of 3PD was an "end around" and whether this would give XPO capabilities beyond what Coyote could provide. In the end, for years now, I have seen a battle set up between XPO and Coyote - two new, fresh and innovative companies in the logistics space. It is refreshing to see these companies grow and lead the industry and I think it is no accident they have taken the industry by storm and surpassed many long standing companies in size. XPO and Coyote are truly innovative and we are watching The Innovator's Dilemma play out in the logistics and supply chain industry - old "mainstream" companies cannot innovate at the pace of these two companies.

However, they now have gone two separate ways. Through the incredible leadership of Bradley Jacobs, XPO is growing through acquisition. They want to own and lead and they are the "hunter".

Coyote has decided (apparently) that the way to grow the company faster and gain more capabilities is to allow itself to get acquired by a much larger company in UPS.

Personally, I think XPO has the right model by keeping control of its fate. As long as the capital is there, I say grow and compete. Don't allow yourself to get swallowed up. Which, I fear, is precisely what will happen to Coyote.

Anyone who has been to Coyote's headquarters knows it is a unique place. As I said above it is all about innovation, working at an incredible pace, young, aggressive and brash. It is an edgy company.

UPS is anything but what I see in Coyote. UPS is deliberate, slow, and measured. It is more about protecting what is than innovating into tomorrow. Perhaps it is possible UPS will truly allow itself to learn from Coyote but business history would say otherwise. Business history would say that UPS will swallow up Coyote and in 5 years we will wonder where it went.

UPS has a big opportunity here and I hope they take advantage of it... Let Coyote be Coyote!

Companies in This post:

Coyote Logistics: www.coyote.com

UPS: www.ups.com

XPO: www.xpo.com

I also questioned in July of 2013 whether XPO's purchase of 3PD was an "end around" and whether this would give XPO capabilities beyond what Coyote could provide. In the end, for years now, I have seen a battle set up between XPO and Coyote - two new, fresh and innovative companies in the logistics space. It is refreshing to see these companies grow and lead the industry and I think it is no accident they have taken the industry by storm and surpassed many long standing companies in size. XPO and Coyote are truly innovative and we are watching The Innovator's Dilemma play out in the logistics and supply chain industry - old "mainstream" companies cannot innovate at the pace of these two companies.

However, they now have gone two separate ways. Through the incredible leadership of Bradley Jacobs, XPO is growing through acquisition. They want to own and lead and they are the "hunter".

Coyote has decided (apparently) that the way to grow the company faster and gain more capabilities is to allow itself to get acquired by a much larger company in UPS.

Personally, I think XPO has the right model by keeping control of its fate. As long as the capital is there, I say grow and compete. Don't allow yourself to get swallowed up. Which, I fear, is precisely what will happen to Coyote.

Anyone who has been to Coyote's headquarters knows it is a unique place. As I said above it is all about innovation, working at an incredible pace, young, aggressive and brash. It is an edgy company.

UPS is anything but what I see in Coyote. UPS is deliberate, slow, and measured. It is more about protecting what is than innovating into tomorrow. Perhaps it is possible UPS will truly allow itself to learn from Coyote but business history would say otherwise. Business history would say that UPS will swallow up Coyote and in 5 years we will wonder where it went.

UPS has a big opportunity here and I hope they take advantage of it... Let Coyote be Coyote!

Companies in This post:

Coyote Logistics: www.coyote.com

UPS: www.ups.com

XPO: www.xpo.com

Wednesday, July 29, 2015

Ben Cubitt From Transplace Interviewed - What Do Carriers Look For in A Shipper

Ben is a very smart person and has been doing this a long time. However, this is another, yet again, "shipper of choice" interview. Some good points are made so I thought I would share it. Although, I must admit, I have no idea what a "fair" rate is especially as it relates to fuel surcharge. Shouldn't a fair fuel surcharge be to just pay what the fuel costs?

Sunday, July 26, 2015

FTR Responds to 10xLogisticsExpert - Are We Driven by Fear

You may have read my blog posting Another Summer and More Fear from FTR. I am happy to link back to the thoughtful and well written response from Jonathan Starks on the FTR Blog entitled "Are We Driven by Fear"?

First, he is right, I read a recap and did not listen to the entire webinar so today I went back and listened to the entire replay. My opinion does not change and here is why.

The point I was making in my post is threefold:

First, he is right, I read a recap and did not listen to the entire webinar so today I went back and listened to the entire replay. My opinion does not change and here is why.

The point I was making in my post is threefold:

- FTR and the "industry" very frequently report "now it is soft" but they predict "sometime in the future" capacity will tighten up and rates will spiral up. (This was exactly the position taken in this webinar)

- They talk about it as if it is very homogeneous when really it is a lane by lane, area by area phenomenon.

- The carriers use this "in the future" research to spin their sales pitch. Any shipper knows the pitch goes something like this:

Shipper to carrier: "Wow, seems real soft now and rates have come down in the spot market (per FTR), what can you do to help lower my contract rates?"

Carrier to Shipper: "Well, yes, may be down now but look at the research (provided by FTR and others), capacity in 2016 is going to tighten dramatically and when that happens rates will spiral up. You, the shipper, need to stick with us now (maybe even give us a cost increase) and we will "stick with you" when spiraling rates occur.

Now, what comes of this:

- Shipper gets scared (thus the fear trade).

- Shipper pays more now as "insurance".

- The "insurance" never pays off (either the spiraling rates never occur or if they do, the carrier is still back at the table asking for more money).

OK, so why am I so skeptical of this scenario? It is really all about who the clients are of any consulting organization. I do not believe you can serve two masters .. absolutely impossible. Yet, some consulting companies try to do this. Imagine this scenario:

Consulting company "A" gets 50% of their revenues from the carriers and is about to go to market with the following research:

- Trucking capacity is loose and rates have softened dramatically

- This is going to exist into the foreseeable future. We are "long" on the recovery and all indications are a recession is upon us (commodities are slowing, etc.).

- Shippers should use this as an immediate opportunity to ask for rate reductions to stay competitive. Prices are about to fall.

What do you think would happen to the "50%" of the revenues that are paid by trucking companies? I will leave you to answer this question.

I want to be clear: I think FTR produces the best research in the industry and it is a "must" listen to and a "must read" for anyone dealing with the shipping industry.

I am merely saying you need to combine this with other research and, more importantly, what you are empirically seeing in the marketplace to determine your overall transportation procurement strategy.

NOTE: My comments about "serving two masters" are the whole idea of where the fiduciary responsibility lies. Think of your investments. If your investment advisor is paid for, in some part, by a specific mutual fund do you think that investment advisory can truly be "neutral" and "agnostic" in his or her advice? Again, I leave it to you to answer.

Saturday, July 18, 2015

DOJ Investigates Airlines - Are the Trucking Companies Next?

A while back I wrote about how I thought executives in the trucking industry were getting dangerously close to collusion as they discussed capacity in the industry. My comments were around a concept of "signaling".

I am not a lawyer and do not pretend to be one but "signaling" is when one company sends a signal to the other about its intents in terms of key actions effecting pricing. So, for example, an executive says in an interview in a prominent industry magazine something like, "Until we see better ROI we cannot and will not add capacity to our system".

Ok, what just happened? He essentially told his competitors two things which normally a company, especially a private one, would want to keep private. He (or She) said: "I am restricting capacity and raising rates". Now, the executive on the other end knows he or she can do exactly the same thing and voila! you know have thinly veiled collusion.

See the graph below, from the article cited below, which displays the profitability of the airline companies who publicly "restrict capacity":

I was thinking about this yesterday as I read in Bloomberg BusinessWeek an article about the FTC complaint against the airlines entitled "What Does it Take To Prove Airline Collusion"? The core of the matter is what they call "unlawful coordination". A line from that article:

At least we have come a long way. Businessweek recounts the following from 1982:

I am not a lawyer and do not pretend to be one but "signaling" is when one company sends a signal to the other about its intents in terms of key actions effecting pricing. So, for example, an executive says in an interview in a prominent industry magazine something like, "Until we see better ROI we cannot and will not add capacity to our system".

Ok, what just happened? He essentially told his competitors two things which normally a company, especially a private one, would want to keep private. He (or She) said: "I am restricting capacity and raising rates". Now, the executive on the other end knows he or she can do exactly the same thing and voila! you know have thinly veiled collusion.

See the graph below, from the article cited below, which displays the profitability of the airline companies who publicly "restrict capacity":

I was thinking about this yesterday as I read in Bloomberg BusinessWeek an article about the FTC complaint against the airlines entitled "What Does it Take To Prove Airline Collusion"? The core of the matter is what they call "unlawful coordination". A line from that article:

"A trigger may have been the June meeting ... where airline executives talked openly about 'capacity discipline', a not so subtle code for limiting the number of seats available" [My comment: thus increasing prices] (Bloomberg Businessweek, July 20, 2015)It went on to say the following:

"At a press conference, Delta President Ed Bastian said his company is "continuing with the discipline the marketplace is expecting". American Airlines CEO Doug Parker told Reuters it was important to avoid over capacity: "I think everybody in the industry knows that." (Bloomberg Businessweek, July 20, 2015)Does any of this sound familiar to the shipping community out there? The DOJ has never really looked at the trucking industry because it was so fragmented. However, is is becoming very consolidated at the top with the top 5 or 10 carriers commanding a huge market share and, of course, if you are a very large shipper, about the only carriers you can use are the very large ones.

At least we have come a long way. Businessweek recounts the following from 1982:

"Robert Crandall of American Airlines told the CEO of Braniff Airlines, Howard Putnam, 'I have a suggestion for you. Raise your goddamn fares 20%. I'll raise mine the next morning. "While doing what is right for drivers and treating people right is the right thing to do (the infamous "shipper of choice" debate), I really think shippers should be far more concerned about this.

Tuesday, July 14, 2015

Upcoming Conferences - Opportunity to Connect

I will be attending the following up coming conferences and look forward to connecting!

CSCMP Annual Global Conference - Sept 27 - 30, 2015

https://cscmp.org/annual-conference

MHI Annual Conference - October 4-6, 2015 (I will be part of a panel titled "The Impact of Automation on Global Supply Chains)

http://www.mhi.org/fall2015/index.cshtml

Look forward to catching up with you all!

CSCMP Annual Global Conference - Sept 27 - 30, 2015

https://cscmp.org/annual-conference

MHI Annual Conference - October 4-6, 2015 (I will be part of a panel titled "The Impact of Automation on Global Supply Chains)

http://www.mhi.org/fall2015/index.cshtml

Look forward to catching up with you all!

Monday, July 13, 2015

The Hoax of the Gartner 25

First, full disclosure: I am a big fan of Lora Cecere so understand I almost always think what she says is big news - I have been following her since her AMR days. Now, having said that, she posted an extremely interesting blog post entitled "Don't Perpetuate The Hoax of The Gartner 25" that is well worth reading.

In fact, I will summarize but clearly you need to go to the post to read the entire entry.

Back when this started, I was actually on the board that voted (AMR days) and I always thought it was moving towards what Lora calls a "beauty" contest and now I believe it is fully just that. Most of it is about brand name recognition. After all, how could a company that so misses demand projections that their new products are unavailable be in the top 25 (Apple) unless it was just brand recognition.

I agree with Lora, to really rate supply chains you have to look at the detailed figures and facts and let the data speak. As she cites in the post, performance + real improvement (in a measurable way), is what should drive the top supply chains.

Go to her blog and give it a read for yourself!

In fact, I will summarize but clearly you need to go to the post to read the entire entry.

Back when this started, I was actually on the board that voted (AMR days) and I always thought it was moving towards what Lora calls a "beauty" contest and now I believe it is fully just that. Most of it is about brand name recognition. After all, how could a company that so misses demand projections that their new products are unavailable be in the top 25 (Apple) unless it was just brand recognition.

I agree with Lora, to really rate supply chains you have to look at the detailed figures and facts and let the data speak. As she cites in the post, performance + real improvement (in a measurable way), is what should drive the top supply chains.

Go to her blog and give it a read for yourself!

Sunday, July 12, 2015

A More Thoughtful Article on Capacity

This, from BCG, is a much more thoughtful article on the true capacity issues in transportation. The issue is NOT trucking capacity as that can easily be solved with private fleets, some technology, moving DCs to more efficient locations etc.

The real issue is around port capacity, rail capacity, infrastructure and consumer demands. These cannot be moved around. And this is what companies have to be thinking about now assuming they want to stay around.

What the trucking companies ignore is the demands being put on transportation are due to rising consumer demands - the demands are not just created by the shipper for the heck of it. My advice is shippers really need to think more about private fleets. You can be very competitive, get higher loyalty from the employees and be far more nimble.

The real issue is around port capacity, rail capacity, infrastructure and consumer demands. These cannot be moved around. And this is what companies have to be thinking about now assuming they want to stay around.

What the trucking companies ignore is the demands being put on transportation are due to rising consumer demands - the demands are not just created by the shipper for the heck of it. My advice is shippers really need to think more about private fleets. You can be very competitive, get higher loyalty from the employees and be far more nimble.

Don't Be Fooled Again..

For those who read my last post and are not sure it is true, I refer you back to the post from November 7th, 2013 titled: "The Fear Trade Picks Up Steam... Don't Be Fooled". Same story from the carriers and the "analysts" (who mostly are just talking their book) just years ago.

And, since it is starting again, I think a great rendition of "Won't Get Fooled Again" is in order:

And, since it is starting again, I think a great rendition of "Won't Get Fooled Again" is in order:

Saturday, July 11, 2015

Another Summer and More Fear from FTR

It is like clockwork. I can set my watch by the articles that will be printed by the logistics' press such as FTR. Here is the story of the "study" (it has been the same for 5 years):

- We thought prices would be a lot higher than they are

- Freight is softer than we thought

BUT.....

- Watch out, it will tighten soon

- Give in to the demands of your carriers as they try to get you to "pre-pay" for price increases.

- Those who do this will be rewarded...

And of course my response continues to be the same: Prepaying for tight capacity is a waste of money. Those who followed this course 3 to 5 years ago have paid a lot of money for a day that still has not arrived.

Actually, you should follow the direction of the executives running these companies: They essentially say when capacity is tight, rates go up and when capacity is loose rates go down. That is the ultimate definition of a commodity. So, therefore, treat it that way.

Wednesday, July 1, 2015

Is Being The Shipper of Choice a Rational Buying Behavior?

I once again had to sit through a "shipper of choice" meeting with a carrier and I was as disappointed as I am with every one of these I attend. First, congratulations to the consultant who coined this phrase "shipper of choice" - you have done a great job peddling this idea and I hope you have made a lot of money with it. Every presentation I go to is the same so I have to believe they emanate from the same person.

For those who have not been "blessed" by one of these presentations, let me walk you through what they mean. In a nutshell it is: "If you (shipper) do everything in the way we want it done, regardless of what your customers want, then you will be a "shipper of choice". Things such as:

For those who have not been "blessed" by one of these presentations, let me walk you through what they mean. In a nutshell it is: "If you (shipper) do everything in the way we want it done, regardless of what your customers want, then you will be a "shipper of choice". Things such as:

- Pay your bills on time

- Give the freight the carrier they are awarded

- Perfectly forecast the freight

- Pay above market (or what the carrier will call "fair") rates

- No window times for deliver - let the carrier deliver and pick up at their leisure

- Have a luxurious wait room for the driver

- Don't have the driver do anything when he shows up

Well, you get the feeling.

What is missing from all of this is what does the CUSTOMER really want? I raised this question to the trucking company and, honestly, I am not sure they ever had thought about this. I mentioned to them that we (the shipper) are not the ultimate customer. We have customers (call them consumers) who are demanding certain things. We are looking for the freight provider to partner with us to fully understand and respond to what the consumer wants (which, as I pointed out to them, is what each of us wants as a consumer). So, what does the consumer want:

- Short order to delivery times

- Windows (anyone want to sit at home all day waiting for someone or do you want to know that they will come within a two hour window)

- Be market competitive in pricing

- Full delivery (White glove).

These are what the consumer wants and these are not things that are being put on the logistics network for any other reason then they are customer demands.

Of course, there are things that make sense and should be done: Pay bills on time, if you award the freight give them the freight etc.

But this idea that we can ignore what the end consumer wants is completely ridiculous. The challenge for us the shipper and the trucking company is how do we meet these complex and ever increasing demands AND be efficient.

I wonder when that meeting will occur?

Tuesday, May 26, 2015

Independent Truckers Pick Up on Mobile Apps

Re-reading a great article from the Wall Street Journal called " Mobile Apps Get Picked Up By Independent Truckers for Better Routes" (Subscription May Be Required). While I am not sure this rises to the level of "Where is Elon Musk in Logistics" (which I asked in my last posting), I do think it is very instructive to see the growth of Mobile Apps in routing trucks. I can remember when people were wondering if they should write computer software for independent truckers because, after all, "how many truck drivers have a computer"?

As silly as that seemed, it is equally silly to believe that truckers will not use Mobile Apps. One of the quotes from the article is from Bryan Beshore, founder of Keychain Logistics:

Here we have "silicon valley" meets the old stodgy trucking industry. And just like every other industry it is the new upstarts who will "disrupt" the industry because the old guard (big brokers) will cater to the allusion of protecting their somewhat bloated bureaucracies and infrastructures.

Look out trucking executives... here come the whiz kids from Silicon Valley!

As silly as that seemed, it is equally silly to believe that truckers will not use Mobile Apps. One of the quotes from the article is from Bryan Beshore, founder of Keychain Logistics:

"I really don’t think that the brokerages serve a huge purpose anymore,”Using geotracking, the smart phone and some really good software it is becoming easier and easier for the independent trucker to cut the middleman (read broker) out of the equation. While this was doable on laptops and regular computers it was just too clunky and hard. With smartphones, and these types of services, an independent truck driver can get their next load in the time it takes to fuel up. This could be real disruptive technology.

Here we have "silicon valley" meets the old stodgy trucking industry. And just like every other industry it is the new upstarts who will "disrupt" the industry because the old guard (big brokers) will cater to the allusion of protecting their somewhat bloated bureaucracies and infrastructures.

Look out trucking executives... here come the whiz kids from Silicon Valley!

Where is The Elon Musk of the Logistics World?

I am currently reading the book Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic Future I highly encourage everyone to read it. However the book gave me pause to think about our industry. An industry that at one time was filled with innovative giants such as Don Schneider and J.B. Hunt. Now, I have to ask, where have they all gone?

I highly encourage everyone to read it. However the book gave me pause to think about our industry. An industry that at one time was filled with innovative giants such as Don Schneider and J.B. Hunt. Now, I have to ask, where have they all gone?

Where is the innovation in logistics and supply chain? Think of it... with all the technology, education and advanced degrees, we still shut down the West Coast ports. And when they shut down, supply chains came to a swift halt.

I consistently hear trucking and intermodal company executives talk about "supply and demand" as a driver of price. They say "Watch out, capacity is low.. prices are going up and you need to be a shipper of choice". Of course, this is nothing more than commodity pricing. They are admitting they are out of ideas and they are pricing their service as a commodity.

In my early days in the industry I was able to see huge risk takers and innovators develop the use of satellite tracking for better routing (Don Schneider) and the proper use of trains and the overall development of intermodal (J.B. Hunt). It was a thrilling time. Lots of change, lots of risk, great growth and huge innovation. Today, it appears innovation is either becoming a broker or buying a company. In some cases, financial engineering has become the innovation of logistics.

I ask, where is our Elon Musk? Where is our Steve Jobs? The industry is screaming for someone to innovate.

Where is the innovation in logistics and supply chain? Think of it... with all the technology, education and advanced degrees, we still shut down the West Coast ports. And when they shut down, supply chains came to a swift halt.

I consistently hear trucking and intermodal company executives talk about "supply and demand" as a driver of price. They say "Watch out, capacity is low.. prices are going up and you need to be a shipper of choice". Of course, this is nothing more than commodity pricing. They are admitting they are out of ideas and they are pricing their service as a commodity.

In my early days in the industry I was able to see huge risk takers and innovators develop the use of satellite tracking for better routing (Don Schneider) and the proper use of trains and the overall development of intermodal (J.B. Hunt). It was a thrilling time. Lots of change, lots of risk, great growth and huge innovation. Today, it appears innovation is either becoming a broker or buying a company. In some cases, financial engineering has become the innovation of logistics.

I ask, where is our Elon Musk? Where is our Steve Jobs? The industry is screaming for someone to innovate.

Monday, May 25, 2015

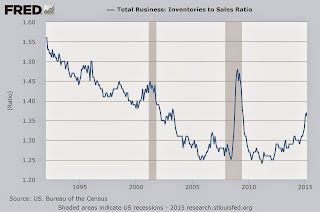

Inventory to Sales Ratio is Not Showing a Pretty Picture - Macroeconomic Monday is Back!

All the data I am seeing is indicating some real softness in the economy. At first, people thought it was the weather and then we went to the port strike. However, now we are starting to see some real convergence of data pointing to a slower economy:

Inventory to Sales Ratio:

As we can see by the FRED graph, this has been on a climb however the slope has increased. Essentially, this is indicating that inventory is building in the supply chain and there is not adequate sell through. Every time this indicator has turned this way, we have seen ultimate softness (as companies work to right size the inventory) and this means softness in the freight markets:

You can see that this is nothing like the spike during the "great recession" however you also clearly can see that when this goes up, recessions do follow (or this is just an indicator of the recession as it happens.

You can see that this is nothing like the spike during the "great recession" however you also clearly can see that when this goes up, recessions do follow (or this is just an indicator of the recession as it happens.

ATA Truck Tonnage Drops in April; Off 5.3% from High in January:

The ATA freight tonnage index peaked in January and has been struggling ever since. While increasing 1% over prior year, it is down 5.9% against previous month, down 5.3% against high in January and indications are the freight index will stay soft. This will drive lower expectations for GDP and, once again, our dream of a year above 3% GDP is starting to fizzle.

While the CASS freight index is still showing some healthy gains in pricing, I really attribute that to the successful "fear mongering" of the carrier base. If buyers of freight truly were objective about the data, they would aggressively be seeking price decreases and not stand for any price increases. This will utimately turn down once the shippers realize what is happening and once the buyers start getting pressured by their managers to adjust the cost basis to reflect what is really happening.

Manufacturer's Alliance for Productivity and Innovation (MAPI) Adjusts Manufacturing Growth to 2.5% From Previous Estimate of 3.5%.

This is a big movement and they attribute this to four key areas from their report:

Without some real big changes, I think we are in for another "sputter" and halt type economy - we are far to used to this now.

Inventory to Sales Ratio:

As we can see by the FRED graph, this has been on a climb however the slope has increased. Essentially, this is indicating that inventory is building in the supply chain and there is not adequate sell through. Every time this indicator has turned this way, we have seen ultimate softness (as companies work to right size the inventory) and this means softness in the freight markets:

ATA Truck Tonnage Drops in April; Off 5.3% from High in January:

The ATA freight tonnage index peaked in January and has been struggling ever since. While increasing 1% over prior year, it is down 5.9% against previous month, down 5.3% against high in January and indications are the freight index will stay soft. This will drive lower expectations for GDP and, once again, our dream of a year above 3% GDP is starting to fizzle.

While the CASS freight index is still showing some healthy gains in pricing, I really attribute that to the successful "fear mongering" of the carrier base. If buyers of freight truly were objective about the data, they would aggressively be seeking price decreases and not stand for any price increases. This will utimately turn down once the shippers realize what is happening and once the buyers start getting pressured by their managers to adjust the cost basis to reflect what is really happening.

Manufacturer's Alliance for Productivity and Innovation (MAPI) Adjusts Manufacturing Growth to 2.5% From Previous Estimate of 3.5%.

This is a big movement and they attribute this to four key areas from their report:

The interesting item of all of this is in item #3 above. Where is all the money gone that the consumer is saving due to low fuel prices? I think it is has gone into the bank or the continued deleveraging of households - meaning people are still not buying.

- Oil and natural gas prices collapsed, causing a sudden contraction of the energy supply chain.

- The strong U.S. dollar reduced growth, a result of cheaper imports to the U.S. and U.S. exports becoming more expensive to foreign buyers, as well as deflation pressure on exports.

- Consumers spent some of their fuel savings in the fourth quarter of 2014.

- The inventory-to-sales ratio rose sharply in the first quarter, while the inventory runoff in the second quarter slowed production growth

Without some real big changes, I think we are in for another "sputter" and halt type economy - we are far to used to this now.

Thursday, April 30, 2015

XPO Logistics Buys Dentressangle - Logistics Companies: Yes, Be Afraid

I have been covering XPO logistics for a very long time on this blog. In that coverage I have evolved my thought from thinking it was just another aggregator that will fail to it being just a big final mile player to finally saying, "watch out", Bradley Jacobs is coming after you.

Yesterday was the deal of the year (in an early year) showing that logistics companies should fear what is going on at XPO. Yesterday, XPO purchased the French company Dentressangle in a deal worth $3.56bl. Now, XPO is clearly a global powerhouse.

At first it looked like XPO was going to be just another big brokerage house. Then came the acquisition of 3PD and rebranding to XPO Final Mile which said they were going to own the delivery from the manufacturer (through brokerage) to your home (through final mile). The next big acquisition in my mind was that of Pacer which immediately made XPO a leader in intermodal.

Now, with the acquisition of Dentressangle they have become truly a global powerhouse. If you are a leader of a global supply chain you absolutely cannot ignore doing business with XPO. The holy grail has been to find a supplier who can do "end to end" supply chain management for your global supply chain and with XPO you most likely have that now.

In all my writings on XPO logistics (which go back to November 19, 2013) I have said they are a force to be reckoned with and now that is clearly come to life.

In full disclosure, I also do business with XPO and I will tell you that the hype is reality. This is a well run, disciplined and well led / well financed company. Trust me - you will do business with XPO at some point.

Yesterday was the deal of the year (in an early year) showing that logistics companies should fear what is going on at XPO. Yesterday, XPO purchased the French company Dentressangle in a deal worth $3.56bl. Now, XPO is clearly a global powerhouse.

At first it looked like XPO was going to be just another big brokerage house. Then came the acquisition of 3PD and rebranding to XPO Final Mile which said they were going to own the delivery from the manufacturer (through brokerage) to your home (through final mile). The next big acquisition in my mind was that of Pacer which immediately made XPO a leader in intermodal.

Now, with the acquisition of Dentressangle they have become truly a global powerhouse. If you are a leader of a global supply chain you absolutely cannot ignore doing business with XPO. The holy grail has been to find a supplier who can do "end to end" supply chain management for your global supply chain and with XPO you most likely have that now.

In all my writings on XPO logistics (which go back to November 19, 2013) I have said they are a force to be reckoned with and now that is clearly come to life.

In full disclosure, I also do business with XPO and I will tell you that the hype is reality. This is a well run, disciplined and well led / well financed company. Trust me - you will do business with XPO at some point.

Sunday, March 29, 2015

Seeking First to Understand in Supply Chain Design

Well, it has been a long time and thank you for all the readers who stayed close to this. I have so many thoughts to write about and I realized when I am not writing I get a bit lazy in terms of researching what best in class people are doing. So, therefore, I need to write.

Today's posting is about "Seeking First to Understand". As Steven Covey told us, when you are engaging with either your team, customers or your spouse for that matter, you should always "seek first to understand". God gave us two ears and one month for a reason. Listen, think and then talk if you have something to say.

How does this relate to Supply Chain Design? Simple, when engaging with a customer or one of your team you should spend the vast majority of your time seeking to understand. Listen to what they have to say, ask probing questions (not yes / no questions but questions that are open ended such as "Tell me More... "Help me understand...") and then think.

If you are formulating a response in your head while someone is talking then I can assure you that you are not listening. Despite popular belief, most people and virtually all minds, cannot multitask while communicating. If you are thinking of your response while the person is talking then you are not listening ... it is that simple.

In Supply Chain design, listening means asking:

Today's posting is about "Seeking First to Understand". As Steven Covey told us, when you are engaging with either your team, customers or your spouse for that matter, you should always "seek first to understand". God gave us two ears and one month for a reason. Listen, think and then talk if you have something to say.

How does this relate to Supply Chain Design? Simple, when engaging with a customer or one of your team you should spend the vast majority of your time seeking to understand. Listen to what they have to say, ask probing questions (not yes / no questions but questions that are open ended such as "Tell me More... "Help me understand...") and then think.

If you are formulating a response in your head while someone is talking then I can assure you that you are not listening. Despite popular belief, most people and virtually all minds, cannot multitask while communicating. If you are thinking of your response while the person is talking then you are not listening ... it is that simple.

In Supply Chain design, listening means asking:

- What are your pain points?

- What are you trying to accomplish with the brand?

- What does the client's or the user of the supply chain customers say and think?

- What does your company want to be known for (for example.. is the competitive advantage being the low cost provider, is it being the high service..i.e. Zappos provider)?

When having one of these sessions you should not respond with immediate ideas but rather with a lot more probing questions. Then, you think.. and that may take days but you think hard. Only then will you be able to formulate a good strategy.

Thinking is hard work and it is tough because, in general, people like to see action (sometimes any action) and thinking is not an outward action. But, trust me, it is the right thing to do.

Monday, December 2, 2013

A Drone Delivers Your Package - Part Deux

Today the logistics world is a buzz with the idea that Jeff Bezos rolled out on 60 minutes last night that a drone could deliver your package.

Too bad 60 minutes did not read this article "A Drone Delivers Your Package" back in FEBRUARY of 2013!

Too bad 60 minutes did not read this article "A Drone Delivers Your Package" back in FEBRUARY of 2013!

Tuesday, November 19, 2013

XPO Finds "The Missing Link" in Big Box Home Delivery - Game Over?

Last week XPO Logistics (See other entries about XPO here) made what I consider a ground breaking announcement and acquisition: They acquired Optima Service Solutions. If you remember, a few months ago XPO purchased 3PD which catapulted the company into the a leading position in big box (Think appliances, home exercise equipment, massive TVs etc.) home delivery. It was a big and bold move to complete the supply chain (They already had services for inbound, redistribution and this gave it "final mile" capability) for XPO.

However, those of us who have been working home delivery (This was a major focus of mine at a major appliance manufacturer) have known for years that the big struggle in this space is in installation and service along with returns. The biggest reason people shy away from internet purchasing of big items (for this example lets say a refrigerator) is because it is so hard to coordinate installation and, if something goes wrong, who do you call? The acquisition of Optima by XPO solves that problem for home deliveries made by XPO / 3PD.

XPO will now have the capability to provide a seamless solution. Before this acquisition the purchase of the refrigerator went something like this:

However, those of us who have been working home delivery (This was a major focus of mine at a major appliance manufacturer) have known for years that the big struggle in this space is in installation and service along with returns. The biggest reason people shy away from internet purchasing of big items (for this example lets say a refrigerator) is because it is so hard to coordinate installation and, if something goes wrong, who do you call? The acquisition of Optima by XPO solves that problem for home deliveries made by XPO / 3PD.

XPO will now have the capability to provide a seamless solution. Before this acquisition the purchase of the refrigerator went something like this:

- You buy from an internet retailer who may or may not coordinate the delivery (some just give you a phone number to a LTL carrier and basically you are on your own).

- The refrigerator is delivered to your curb (many will only do curbside deliveries).

- The driver may or may not help you unload (many LTL carriers will tell you that you have to unload the refrigerator yourself).

- The driver leaves and now you and your wife stare at this new beautiful refrigerator sitting in your garage and your wife says to you, "What the hell are we going to do with that"?

Now think of the "new world" of big box deliveries (again, our fictional refrigerator) with the integrated and seamless solution XPO will offer:

- You choose an internet retailer specifically because they have the XPO / 3PD / Optima team as their delivery agent (Same refrigerator but this retailer is preferred due to the delivery mechanism).

- When you coordinate the delivery you tell them you want it fully installed and the installation is seamlessly scheduled for you.

- When the driver shows up to deliver the refrigerator the installation technicians arrive at the same time and they take over.

- Your refrigerator is installed, icemaker tested, etc. etc.

- You and your wife look at the beautiful new refrigerator where it belongs - installed and ready to be used.

This is why this acquisition is so important. The complexities of buying a big box item over the internet are lifted from the consumer and put where they belong - on the delivery agent. No one has been able to do this better than Optima and now Optima is exclusively part of the XPO / 3PD network.

Bradley Jacobs has, in one masterful stroke, accomplished two great things for his company. First, he has given the company the ability to make a seamless end to end solution for home delivery all the way through delivery and service. Second, and probably as important, he took the leader of this service, Optima, off the market for other home delivery agents. Now, if you were a local home delivery agent and behind the scenes you were using Optima, you will no longer be able to do to that as Optima is exclusive to 3PD.

This is the equivalent of a "Pick 6" in football. Your great defense not only makes a great defensive play but it also scores a touchdown.

The last frontier for potentially preventing people from buying big box items over the internet is now just returns - and don't bet against XPO in this space - they will figure it out.

Wednesday, November 13, 2013

Rethinking The Core Carrier Strategy - Too Many Eggs in One Basket?

There are two sides of a continuum in procurement strategies for transportation. On one end is full "auction" type purchasing where you put everything out to bid, almost constantly, and let the market adjust the prices. On the other end is single sourcing where you don't bid anything and you partner with a core company.

Close to sole sourcing is a strategy called "core carrier". This strategy has you limit your carriers to a "vital few" and then you work with them. Sounds great however lately I have seen this degenerate to what is virtually a sole source strategy. So, what is wrong with this and is it time to rethink it? It appears Amazon thinks so.

As I wrote on Monday, Amazon is teaming up with the United States Postal Service (USPS) to execute Sunday deliveries. Sounds great and the possibility of this occurring I wrote about back in 2012 but there may be more to this. In The Wall Street Journal's "Heard on the Street" column (subscription required) they mention how this may actually be a strategic decision to ensure they have options beyond FEDEX and UPS.

In conjunction with their private fleet for grocery deliveries, Amazon appears to be diversifying and growing their options. A real strategic risk for Amazon is they become so beholden to Fedex and UPS that they are controlled by them. This strategy appears to be their attempt to counter that risk.

For the average shipper you should be thinking about this strategy as well. Initially the idea of sole sourcing or core carrier sounds great - low administrative costs, one point of contact, easy to do business with. Long term, however, you have to ask yourselves if you are turning the keys to the kingdom over to someone who many not have your best interest in mind. No fault of their own but their interest will always be in the profitability of their company. So, here are some actions you should be thinking about to protect the long term ability of your company to execute their strategy:

Close to sole sourcing is a strategy called "core carrier". This strategy has you limit your carriers to a "vital few" and then you work with them. Sounds great however lately I have seen this degenerate to what is virtually a sole source strategy. So, what is wrong with this and is it time to rethink it? It appears Amazon thinks so.

As I wrote on Monday, Amazon is teaming up with the United States Postal Service (USPS) to execute Sunday deliveries. Sounds great and the possibility of this occurring I wrote about back in 2012 but there may be more to this. In The Wall Street Journal's "Heard on the Street" column (subscription required) they mention how this may actually be a strategic decision to ensure they have options beyond FEDEX and UPS.

In conjunction with their private fleet for grocery deliveries, Amazon appears to be diversifying and growing their options. A real strategic risk for Amazon is they become so beholden to Fedex and UPS that they are controlled by them. This strategy appears to be their attempt to counter that risk.

For the average shipper you should be thinking about this strategy as well. Initially the idea of sole sourcing or core carrier sounds great - low administrative costs, one point of contact, easy to do business with. Long term, however, you have to ask yourselves if you are turning the keys to the kingdom over to someone who many not have your best interest in mind. No fault of their own but their interest will always be in the profitability of their company. So, here are some actions you should be thinking about to protect the long term ability of your company to execute their strategy:

- Be careful on too much concentration in one carrier - especially intermodal

- Ensure suppliers know (and it is believable) that you have options in the market place.

- Be careful of tying systems together which are core to your business. Beyond EDI, once their are unique systems integrations you are married (sometimes for life).

- Think about strategically propping some carriers up to ensure they are competitive. Think about Amazon and the USPS. Why go with what is essentially a bankrupt carrier? Amazon wants to keep them in business and is going to help them. You may have to do that with some smaller carriers yourself.

- Keep options open with private fleet. By running a private fleet you will know as much or more about running a fleet than your suppliers. Keep that as a competitive advantage.

As always, there is a lot to learn from Amazon.

Tuesday, November 12, 2013

Behind The 2.5% GDP Number.. Not So Fast

The initial read on Q3 GDP seemed pretty impressive at 2.5%. That would indicate things are moving along and creeping up to the 3% "benchmark" everyone is waiting for. However, like all things, there are the numbers then there are the numbers.

I had heard on NPR that the inventory numbers seemed elevated so I did some quick research and sure enough it appears that at least .5% of the GDP number was due to the growth in inventory. Of course, making things and throwing them in warehouses is not a driver of growth. It is more like a ponzi scheme.

Forbes said the following:

What are the implications for shippers and transporters:

I had heard on NPR that the inventory numbers seemed elevated so I did some quick research and sure enough it appears that at least .5% of the GDP number was due to the growth in inventory. Of course, making things and throwing them in warehouses is not a driver of growth. It is more like a ponzi scheme.

Forbes said the following:

"When you remove inventory accumulation and external trade, explains Capital Economics’ Chief US Economist Paul Ashworth, you get a slowing 1.7% growth rate of final sales to domestic purchasers. Ashworth calls this less impressive metric “a better gauge of underlying economic strength.”

What are the implications for shippers and transporters:

- The economy is not growing like the front page numbers may imply. Things are sluggish for the most part with some strength industries - although those are not big freight industries.

- Due to the growth in inventory, there has been a "pre-positioning" that will have to bleed off. This means, at some point, inbound freight will slow down dramatically waiting for the inventory to be sold.

- Nothing indicates freight will speed up. This slow freight environment which means demand is decreasing at least as fast as supply will be the "new normal" for at least one year.

Everything I read and see says this slow "new normal" freight environment will go through 2014 at a minimum.

Lesson: Always read "behind" the numbers.

Subscribe to:

Posts (Atom)